Forefront | Blog

Q2 M&A Market Roundup

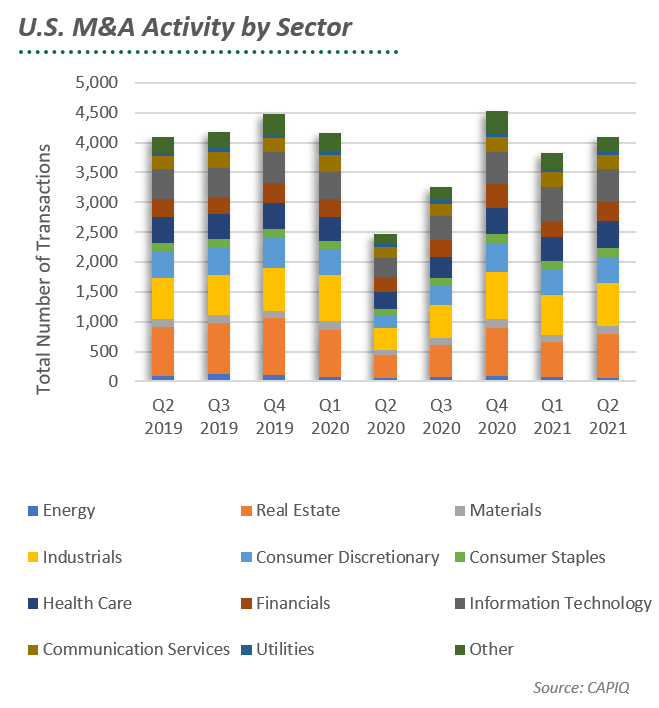

M&A activity in the United States at the end of Q2 2021 has continued to recover from previous pandemic induced lows. According to M&A transactional data derived from CAPIQ, total U.S. M&A deal activity has improved year over year. Total closed M&A transactions, including both public and private companies, has increased approximately 65% when comparing Q2 of 2021 to Q2 of 2020. At the end of the first half of 2021, deal volumes are approximately 19% higher than they were in the first half of last year. This alone points to an M&A market that has strong momentum heading into the second half of 2021.

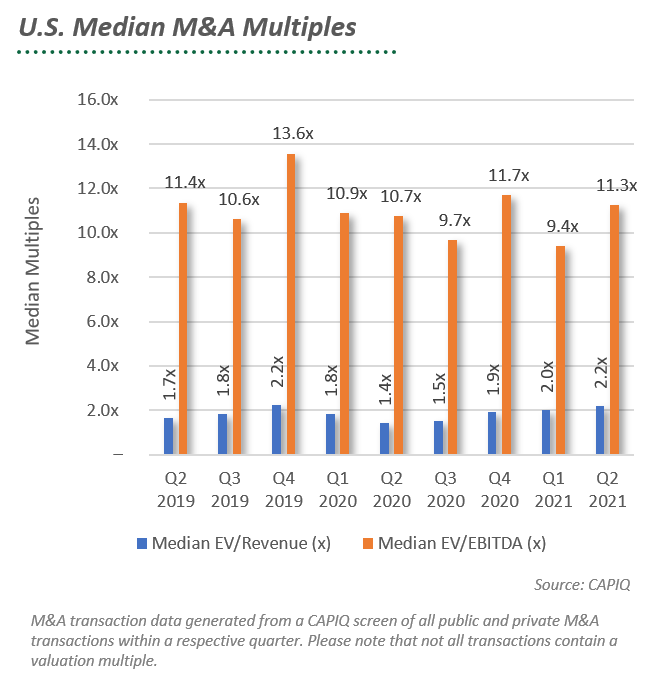

In addition to robust deal volumes, valuations continue to remain high as evidenced in the “U.S. Median M&A Multiples” chart below. The median Implied Enterprise Value/EBITDA for private and public M&A transactions has risen from 10.7x in Q2 of 2020 to 11.3x in Q2 of 2021. The median Implied Enterprise Value/Revenue has risen as well from 1.4x in Q2 of 2020 to 2.2x in Q2 of 2021.

Q2 M&A Trends

The effect of higher inflation on the economy was highly debated in Q2. Despite fears that the Federal Reserve could potentially raise rates, Federal Reserve Chairman Jerome Powell reassured dealmakers when he “repeatedly emphasized he still expects price pressures to ease later this year” during the Fed’s semi-annual report to House lawmakers, reported the Wall Street Journal. While interest rates continue to remain low an uptick in inflation, beyond the Fed’s comfort levels, could result in the Fed raising rates unexpectedly. This would be a tough pill to swallow for the U.S M&A market if it were to occur.

In addition to inflation, we continued to see tight labor markets and global supply chain disruption during Q2. This could end up interfering with dealmaking in industries where these costs are crucial to the businesses that make up those industries in the second half of 2021.

The proposed increase of both the corporate tax rate, from 21% to 28%, and marginal capital gains rate, from 20% to 39.6%, influenced M&A markets in Q2. PitchBook reported that the rumored increase in the marginal capital gains tax rate “is spurring many family-owned businesses to consider selling one to three years ahead of schedule to prevent paying higher taxes on a sale.” Overall deal volumes in Q2 were most likely affected by this and will likely continue to have an impact as the tax legislation progresses.

U.S. M&A Outlook for Second Half of 2021

As evidenced in both Q1 & Q2 of this year, the M&A market is experiencing a rebound from the lows of 2020. It is safe to expect that the prevailing concerns of inflation, labor shortages, supply chain disruption, and a tax increases will continue to be a concern for the M&A market as we move into the second half of 2021. There is still an abundance of capital on the sidelines with more willing sellers due to potential tax changes. The first half of the year has been strong for the M&A market and will likely continue as we make our way through the rest of 2021.