Forefront | Blog

First Half of 2024 M&A Market Review

2023 M&A Market Recap

In 2023, the M&A market was somewhat muted. Total deal value amounted to $1.766 trillion, representing an 8.5% decrease compared to the previous year, reflecting a generally tough year. The number of transactions also fell significantly, with 15,893 deals completed, down 15.8% year-over-year. This decline, occurring for the second year in a row, can be attributed to several factors:

- Stricter monetary policies resulting in higher interest rates.

- A growing disparity in valuation expectations between buyers and sellers.

- Increased geopolitical tensions.

However, these challenges seem to be easing somewhat as inflation subsides and interest rates are anticipated to decrease in 2024. While geopolitical tensions and recession risks still pose uncertainties, the most difficult period may be behind us.

First Half of 2024 M&A Overview

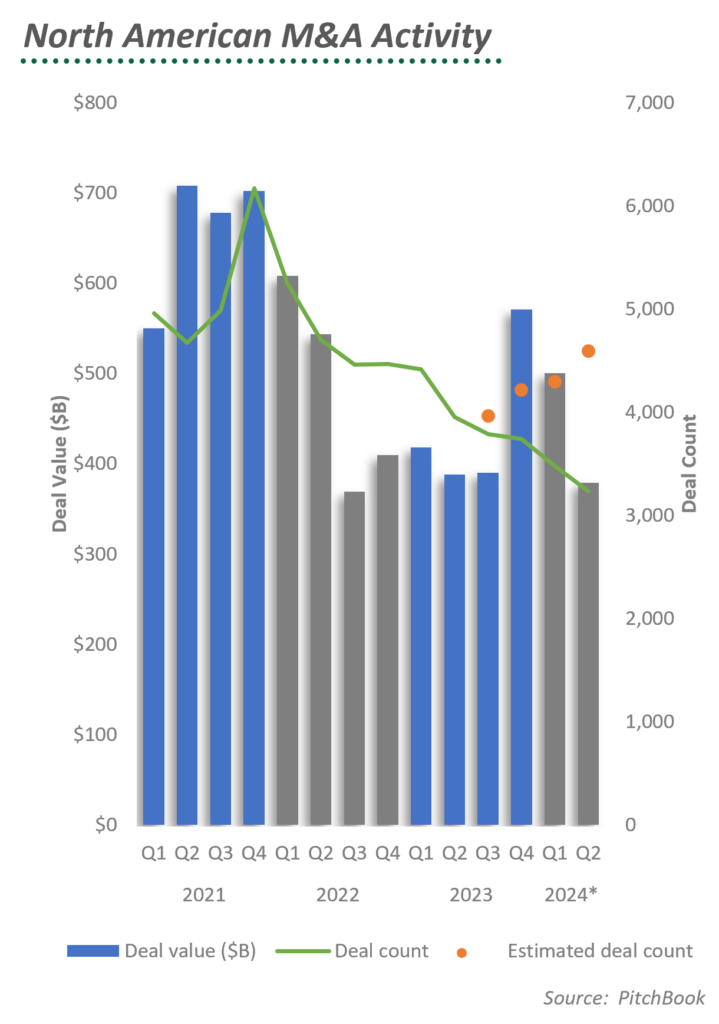

Global deal value rises YOY for the third consecutive quarter, despite a 13.5% drop in deals since Q2 2023.

- The 616 global IPOs in H1 2024 were fewer than the 674 in H1 2023 and 872 in H1 2022.

In the first half of 2024, North American M&A activity saw a notable increase of about 13.0% year-over-year, in both deal count and value. By the end of this period, deal value is expected to exceed $975 billion, with nearly 9,000 deals announced or completed. Although activity in Q2 slightly tapered off from Q1, the overall performance in the first half of 2024 was significantly stronger than the previous year. Anticipation of lower interest rates later in the year is fueling optimism for a resurgence in deal-making.

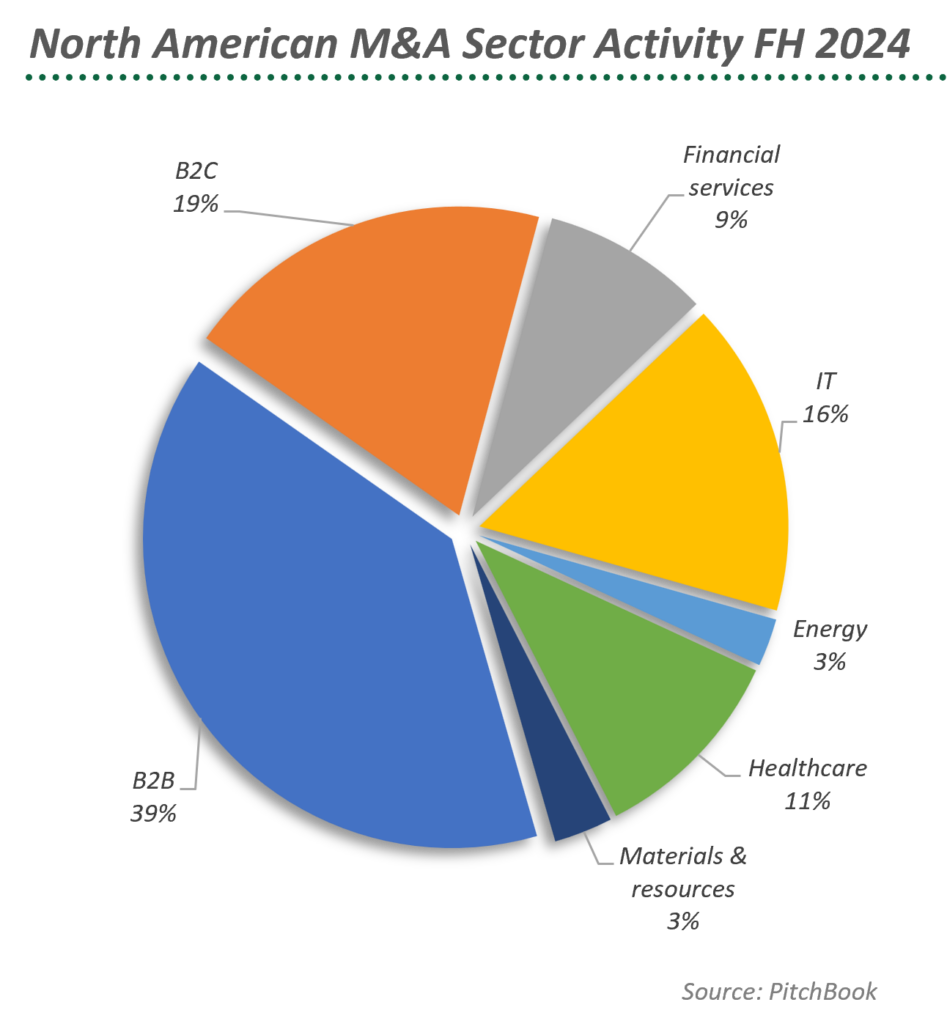

The top 10 North American deals in Q2 amounted to $106.0 billion, marking a 32.1% year-over-year growth. This quarter’s largest deals were smaller compared to those in Q1. The leading sectors in these top deals were energy and IT, each with three transactions, followed by business services with two deals, and one deal each in healthcare and financial services.

There was a notable rise in private equity (PE) sponsor-backed deals, with half of the top 10 deals being PE-backed.

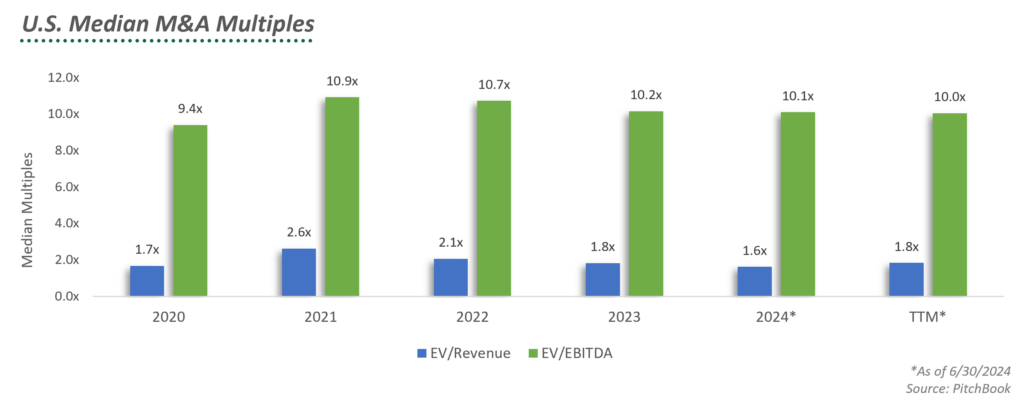

The average median revenue and EBITDA multiples across all sectors, on a trailing twelve-month (TTM) basis at the end of Q2 2024, were 1.8x and 10.0x, respectively.

First Half of 2024 M&A Trends

PE portfolios are primed for sale. At the start of the year, PitchBook reported that PE firms globally held over 27,000 portfolio companies, with roughly half having been owned for at least four years—an optimal time for exits. By mid-2024, many of these investments have aged an additional six months. PE firms currently raising new funds face investor scrutiny over limited returns, intensifying the pressure to sell. Failure to distribute returns from existing investments could hinder their ability to secure new capital.

Corporates are pursuing transactions to drive growth and transformation amid a more disruptive and uncertain environment. With challenges from macroeconomic shifts, geopolitical tensions, and technological advances—especially AI—companies need to innovate and adapt. Those with strategic M&A plans to acquire key capabilities, talent, and technology, or divest non-core assets, will be best positioned for success.

AI, especially generative AI, is set to drive various transaction types and disrupt businesses and entire industries. Though still in its early stages, AI is already significantly impacting cost efficiencies, revenue streams, customer channels, and value propositions. As AI reshapes the landscape, companies will need to reassess their strategies, business models, and market positions. This shift may lead to a range of transactions, including traditional M&A, partnerships, and novel collaborations.

Inorganic growth is necessary to counter weak organic growth. With macroeconomic conditions and monetary policies leading to sluggish economic expansion, achieving organic revenue growth has become challenging. As a result, companies may need to rely on M&A to boost their revenues.

The downturn is affecting PE firms more than corporates. With M&A activity involving financial sponsors dropping 34% in the first half of 2024 compared to an 18% decline for corporates. As a result, corporates’ share of M&A activity has risen from 60% to 63%, partly due to their lower reliance on debt.

M&A Outlook for Remainder of 2024

All things considered, there is a positive outlook for deal activity, driven by ongoing digitization and advancements in AI. Technological acquisitions, ESG goals, decarbonization, and energy transition are expected to fuel many transactions in the coming years. Companies will also pursue transformational deals to strengthen resilience and address capital scarcity.

M&A is now a key strategy for CEOs aiming to achieve growth and transformation goals. Despite clear motivations, the timing of deals is influenced by factors like capital availability and macroeconomic conditions. Private equity firms and large corporations have significant capital to drive deals, while others may rely on divestiture proceeds.

Current favorable conditions include lower interest rates and a recovery in sector valuations, which facilitate negotiations. However, dealmakers must navigate ongoing regulatory changes, geopolitical tensions, and complex national election outcomes.

Overall, while the M&A market in the second half of 2024 may face challenges, opportunities driven by technological innovation, strategic acquisitions, and capital availability will likely sustain robust deal activity.

Source: PitchBook, PWC & BCG