Forefront | Blog

Maximizing Profitability During a Supply Shortage

Companies of all shapes and sizes seem to be experiencing shortages in materials/labor nowadays. It’s headline news that just doesn’t want to go away. Companies do not have the resources to meet all the volume demanded by their customers. Some volume trade-offs must be made, and companies face decisions of which products to produce and sell. So, how should a company determine which opportunities to pursue, and which ones to reject? Obviously, there are a myriad of factors to consider, primarily maintaining long term profitable relationships with customers. Mitigating financial shortfalls during these times can be difficult while trying to meet this goal. A contribution margin analysis (Sales – Variable Expenses) of the constrained resource is a key tool during a shortage and can be applied in a couple ways to help maximize profitability.

The first application is used in determining how to allocate the resource among products and customers. A company’s instinct may be to focus on selling goods with the highest contribution margin at the product level. However, a deeper dive into the contribution margin of the constrained resources (materials, and/or labor, etc.) is necessary.

Let’s look at the following example:

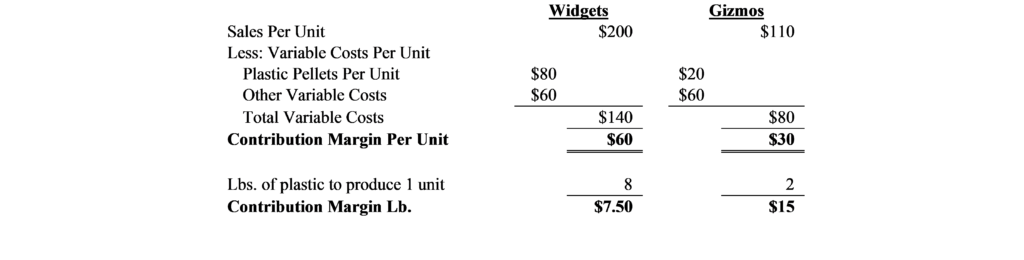

Tier II Company manufacturers widgets and gizmos. Both products require plastic pellets costing $10 lb. for their production. Widgets require 8 lbs. of pellets, and gizmos require 2 lbs. of pellets. Fixed costs remain the same regardless of how many units produced and sold and therefore are irrelevant to the calculation to maximize profitability. There is a demand of 1,000 widgets, and 1,000 gizmos. However, Tier II can only obtain 4,000 lbs. of plastic pellets through its normal supplier. Contribution margins per product unit and per pound are shown in the table below….

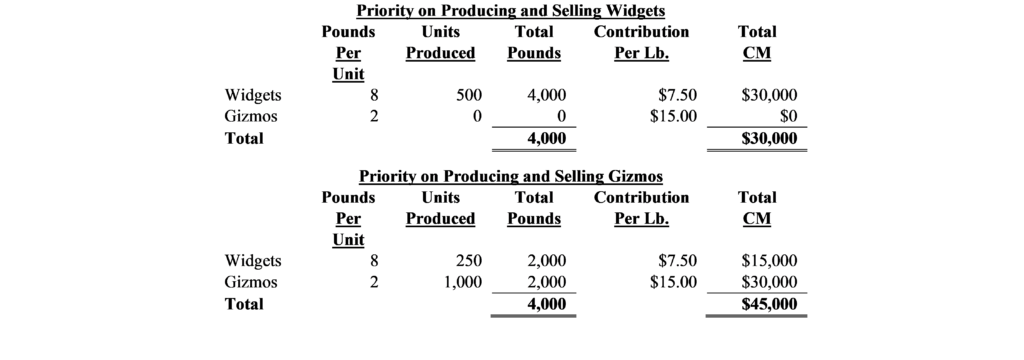

On the surface it appears that at a contribution margin of $60 per unit, producing and selling widgets would be more profitable than gizmos at $30 per unit. Focusing more closely on the contribution per pound reveals that using up the constrained resource of 4,000 lbs. of plastic on widgets would be detrimental to profits. The analysis in the table below shows that prioritizing production and sales of gizmos as being more profitable.

Although there are a myriad of factors and considerations, this simple contribution margin analysis of the item(s) in short supply provides extremely valuable insight in making the right decisions to maximize profitability during those critical times.